Quick Answer: Prop Trading in Germany

- • Prop trading is legal in Germany. BaFin does not regulate retail prop firm challenge accounts because they're simulated, not real brokerage accounts.

- • Prop firm payouts are taxed as sonstige Einkünfte (other income) under §22 EStG in most cases, not as Kapitalerträge (§20 EStG) or Gewerbeeinkünfte (§15 EStG).

- • You do NOT need a Gewerbeanmeldung to trade with a prop firm, unless the Finanzamt classifies your activity as gewerblich based on volume and frequency.

- • Every major prop firm accepts German traders. SEPA transfer, Rise, or crypto make collecting payouts straightforward from a German bank account.

- • The biggest mistake German traders make is ignoring the tax question until the first payout hits. Talk to a Steuerberater before your first withdrawal, not after.

Prop trading is legal in Germany, BaFin doesn't regulate retail challenge accounts, and your payouts are most likely taxed as sonstige Einkünfte under §22 EStG at your personal income tax rate. That's the short version. The rest of this article is the long version.

I'm Paul. I trade with 50+ prop firms from my desk in Germany, I've collected payouts from over a dozen of them into my German bank account, and I've dealt with the Finanzamt along the way. If funded trading is new to you, start with what a prop firm actually is. This guide covers the Germany-specific part.

The confusion around prop trading in Germany comes down to three things: BaFin, taxes, and the Gewerbeanmeldung question. I'll cover all three with real experience, not copy-pasted legal disclaimers.

Does BaFin Regulate Prop Trading Firms?

No. BaFin (Bundesanstalt für Finanzdienstleistungsaufsicht) regulates banks, brokers, insurance companies, and investment firms operating in Germany. Prop firms offering funded trader challenges don't fall under BaFin's jurisdiction because they're not offering financial services to German consumers.

When you sign up for a prop firm evaluation, you're paying for a performance assessment. The account is simulated. You're not opening a brokerage account, not depositing margin, not trading real capital from a regulated entity. As of March 2026, no major prop firm holds a BaFin license, and none need one. The firms operate from the US, UK, UAE, or offshore. BaFin has not issued specific guidance on retail prop firm challenges, and there's no indication they plan to.

BaFin has been active against unregulated CFD brokers and forex scams. If a prop firm were actually holding customer funds or offering leveraged financial products to German residents, that would trigger regulatory requirements. The simulated-account model specifically avoids this.

Does this mean zero consumer protection? Essentially, yes. You're relying on the firm's reputation, payout track record, and contractual terms. No German regulator will step in if a firm refuses your payout. Due diligence is on you.

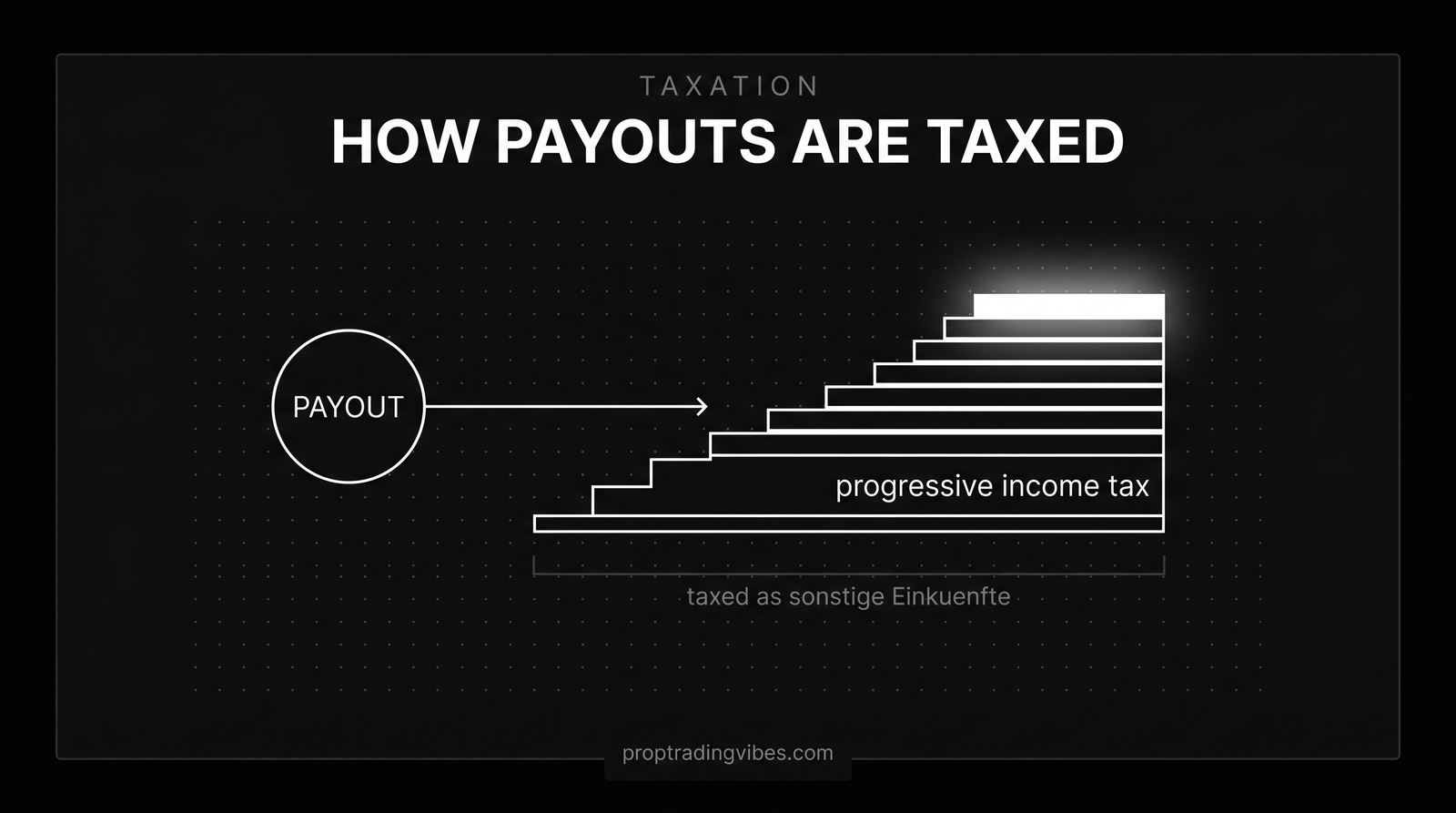

How Are Prop Trading Payouts Taxed in Germany?

Prop firm payouts are most commonly taxed as sonstige Einkünfte under §22 EStG, at your personal income tax rate. The answer is more nuanced than you'd expect because German tax law wasn't written with prop firm payouts in mind.

The Three Possible Tax Categories

§20 EStG, Einkünfte aus Kapitalvermögen (capital income). This is where normal trading profits go. If you trade your own retail brokerage account, profits are taxed at a flat 25% plus Solidaritätszuschlag and potentially Kirchensteuer, roughly 26.4% effective (27.8% with Kirchensteuer). Prop firm payouts likely don't qualify here. You're not trading your own capital. You're receiving a performance-based payment from a company.

§15 EStG, Einkünfte aus Gewerbebetrieb (business income). Applies if the Finanzamt classifies your prop trading as a commercial activity. That triggers Gewerbesteuer on top of income tax, and you'd need a Gewerbeanmeldung. High frequency, significant revenue, and running it like a business can push you into this category.

§22 EStG, Sonstige Einkünfte (other income). The most common treatment for prop firm payouts based on what I've seen from other traders and tax advisors in the space. You're receiving income from a contractual relationship with a foreign company, not capital gains from your own invested capital, and for most traders it's not yet a full-blown Gewerbe. Taxed at your personal income tax rate, 14% to 45% depending on total income.

| Tax Category | Rate | When It Applies | Prop Firm Relevance |

|---|---|---|---|

| §20 EStG (Kapitalerträge) | ~26.4% flat | Trading your own capital in a brokerage account | Unlikely, you're not trading your own capital |

| §22 EStG (Sonstige Einkünfte) | 14-45% progressive | Contractual performance-based income from foreign entities | Most common treatment for occasional payouts |

| §15 EStG (Gewerbeeinkünfte) | 14-45% + Gewerbesteuer | Activity qualifies as a trade or business | Possible if high volume, multiple firms, primary income |

The critical difference: §20 EStG is flat at ~26.4%, while §22 and §15 use your progressive rate. If you're making significant prop income on top of a day job, your marginal rate can hit 42% quickly. For context on what realistic prop income even looks like, see my breakdown of prop trader salary.

My actual setup: I report prop firm payouts as sonstige Einkünfte. My Steuerberater has confirmed this treatment for my specific situation. But I am not your Steuerberater. Your situation might differ, especially if prop trading is your primary income source.

How to Report It on Your Einkommensteuererklärung

- Collect all payout records. Download statements from each firm dashboard. Note date, USD amount, and EUR amount received.

- Convert foreign currency. If you received USD directly, use the ECB reference exchange rate for the day of payment.

- Fill out Anlage SO (Anlage Sonstige Einkünfte). This is where §22 EStG income goes. If your Steuerberater classifies it differently, they'll redirect it to the appropriate Anlage.

- Deduct Werbungskosten. Subtract evaluation fees, platform subscriptions, and data feeds in the Werbungskosten section of Anlage SO.

- Handle double taxation. Germany taxes worldwide income, but most prop firms sit in jurisdictions with no withholding tax on payments to German residents. If a firm withholds tax (unusual), claim it on Anlage AUS.

If the Finanzamt Asks Questions

Be prepared, be organized, don't panic. Traders do receive a Rückfrage about foreign income entries. The response is straightforward: prop trading is a performance-based contractual relationship with a foreign company, you trade simulated accounts, and you report the income accordingly.

Keep on file: the firm's contract or terms of service, payout statements for every withdrawal, evaluation fee receipts, bank statements, and a one-page summary in German explaining the business model. The Finanzamt isn't hostile toward prop trading. Transparency and documentation solve 95% of potential issues. One more thing I've learned: they care about consistency. File your income the same way every year, and get the classification right from the start.

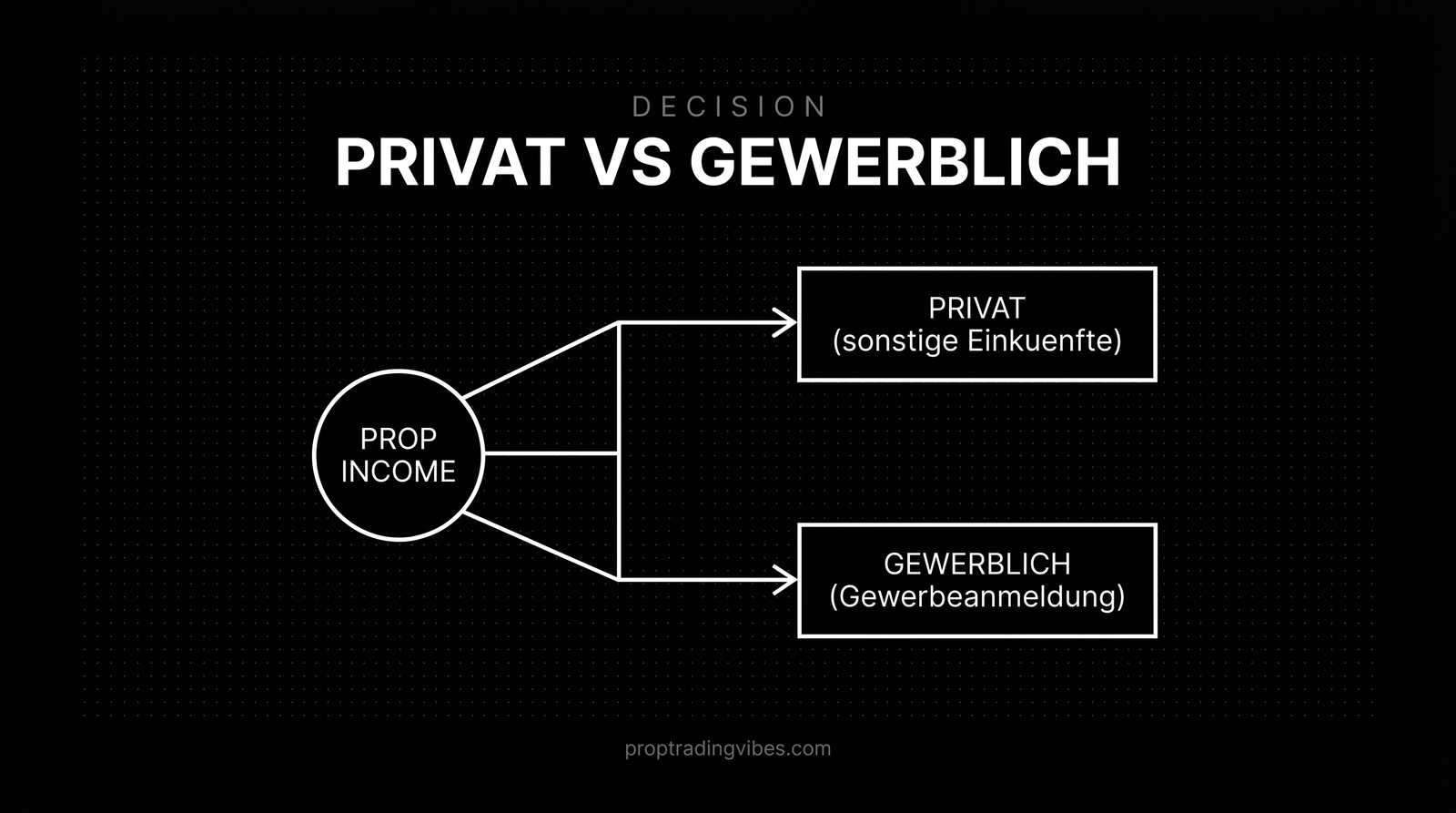

Do You Need a Gewerbeanmeldung for Prop Trading?

Probably not, but it depends on how much you're making and how the Finanzamt views your activity.

A Gewerbeanmeldung (business registration at your local Gewerbeamt) is required when your activity qualifies as a Gewerbe under German commercial law: independence, sustainability, intent to profit, and participation in general economic exchange. Prop trading checks most of those boxes. The question is whether it crosses from a side activity into a full commercial operation.

If you're collecting $500 payouts from one firm every few months, no Finanzamt in Germany will classify that as a Gewerbe. Running 15 funded accounts across 5 firms, pulling in $5,000+ per month as your primary income? Different story. That's trading for a living territory, and the tax setup needs to match.

The practical advice: start without a Gewerbeanmeldung and report under §22 EStG. If your revenue grows consistently above roughly €2,000/month, ask a Steuerberater whether registration makes sense. Some traders actually prefer it, because a Gewerbe lets you deduct software, data feeds, and evaluation fees as Betriebsausgaben.

Are Evaluation Fees Subject to VAT (Umsatzsteuer)? Plus What You Can Deduct

For private individuals, no German VAT is owed on evaluation fees. Most prop firms are based outside the EU, and when a German trader pays a US-based or UAE-based firm, reverse charge under §13b UStG would apply, but only to registered businesses. Without a Gewerbeanmeldung and USt-IdNr, the mechanism doesn't apply to you. The fee is simply a cost of participation.

If you DO have a Gewerbeanmeldung, you'd self-assess VAT at 19% on the fee and claim it back as Vorsteuer in the same filing. Net effect: zero. But the paperwork is real, a monthly or quarterly Umsatzsteuervoranmeldung. My take: the VAT situation is a non-issue for 90% of German prop traders because most don't have and don't need a Gewerbe.

What You Can Deduct as Werbungskosten

Reporting under §22 EStG, you can deduct directly related expenses, which reduces your taxable payout amount:

- Evaluation fees. If you failed five evaluations at $150 each before passing one, that's $750 in deductible costs. Failed attempts count too, because they're directly tied to earning the income. (Keeping fees low helps regardless, see cheapest prop firms.)

- Data feeds and tools. Rithmic or CQG subscriptions, TradingView Pro, NinjaTrader licenses, journaling tools like Tradervue.

- Education. Courses, books, coaching, but only with a direct connection to your prop income. The Finanzamt isn't generous here, so keep receipts.

- Hardware. A trading monitor, internet upgrade, or computer used primarily for trading. Mixed personal/trading use gets a proportional deduction.

The constraint: your total Werbungskosten must exceed the Pauschbetrag (flat deduction of €1,230 as of 2026) before itemizing gains you anything. For active traders, evaluation fees alone often clear that threshold.

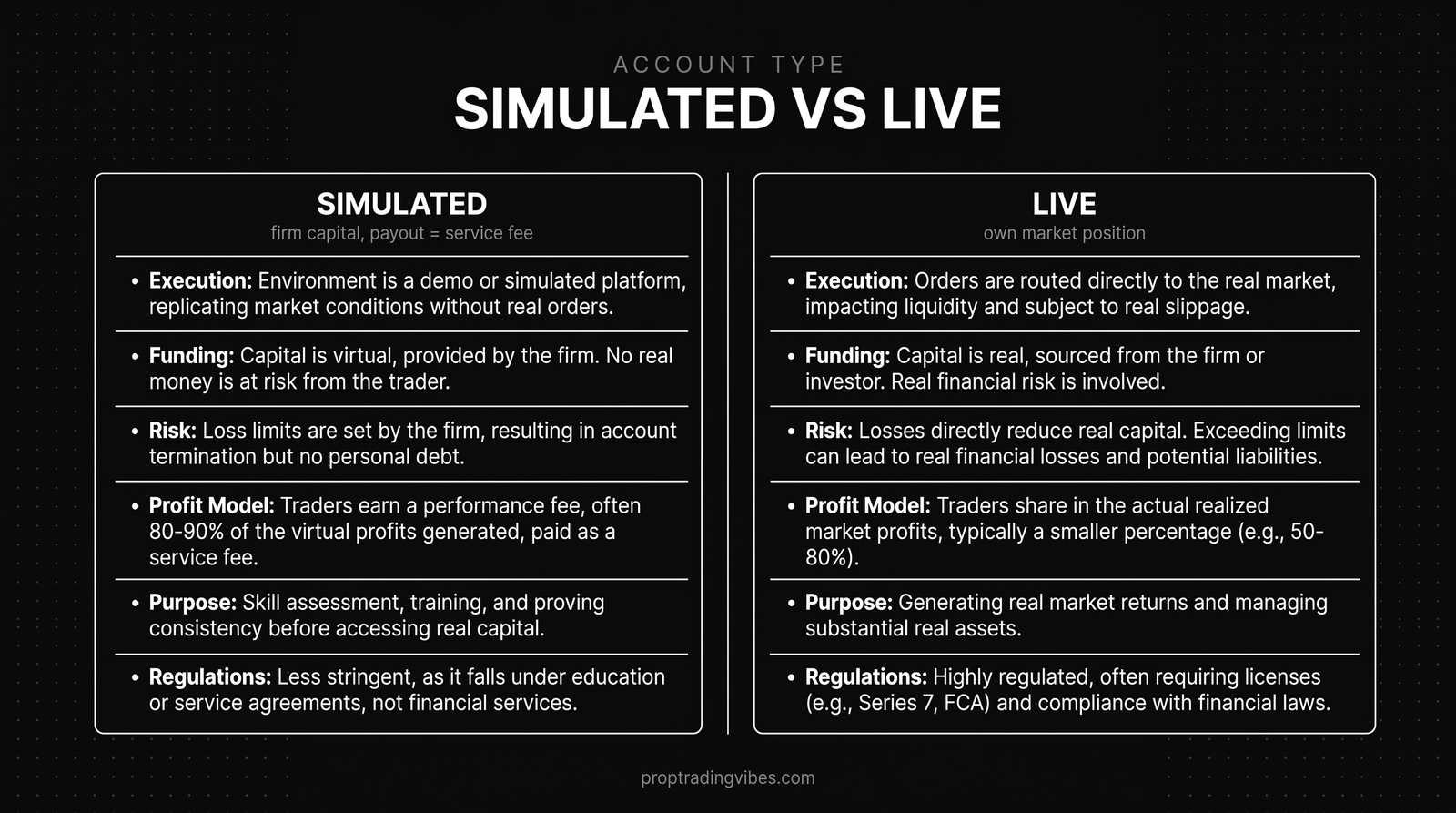

Simulated vs. Live Accounts: What It Means for German Tax Law

Almost every prop firm in 2026 uses simulated accounts. You're not placing real orders on CME or Eurex. The firm gives you a demo account, mirrors your trades, and pays a profit split from its own revenue model. (More on that in how prop firms make money.)

This matters for German tax law because it reinforces the argument that payouts are NOT Kapitalerträge under §20 EStG. You never invested capital. You never held a financial instrument. You received a contractual performance payment, similar to a freelance consulting fee, except the "consulting" is your trading skill.

Some traders worry simulated accounts look less legitimate to the Finanzamt. I've found the opposite. Because it's clearly not a brokerage relationship, the treatment is cleaner. No confusion about whether the 25% Abgeltungssteuer applies. It doesn't. You report the income, deduct your evaluation fees, and pay your personal rate.

The exception worth knowing: a few firms (rare in 2026) still offer live funded accounts where real capital is deployed. If you trade real capital through a firm and receive a profit share, the §20 EStG argument gets stronger. But that's an edge case in the retail prop space.

The Steuerberater Question: When Do You Need One?

The moment you receive your first payout, you should have a Steuerberater lined up who understands trading income. Not next year. Now.

The problem in Germany is finding one who actually understands prop trading. Most tax advisors have never heard of funded trader programs. You'll spend the first 30 minutes explaining why the account is simulated and why a UAE company is sending you USD.

My tip: look for a Steuerberater who works with freelancers or digital entrepreneurs. They're used to foreign income and unusual business models. Ask directly whether they've handled prop trading income before. A no is fine, as long as they'll research it rather than defaulting to §15 EStG and triggering the Gewerbeanmeldung cascade.

A good one will classify your income correctly, set up quarterly Vorauszahlungen so you don't get hit with a massive bill in May, advise on the Gewerbe question, and help you track deductions. Expect €200-500 for an initial consultation and €800-1,500/year for ongoing filing in a straightforward situation. Worth every cent compared to getting the classification wrong.

Which Prop Firms Work Best from Germany?

Every major prop firm accepts traders from Germany. I've never been rejected based on my German address or passport, and the rules are identical no matter where you trade from. KYC is painless: a German Reisepass or Personalausweis works everywhere, some firms add a utility bill for address proof, and verification typically takes 24-48 hours. Firms like Tradeify have paid out to German bank accounts without friction. Where a firm is based matters for contract law, not for access.

The real differences are payment methods:

- SEPA transfer. The gold standard. Direct EUR into your Girokonto, no conversion fees on your end, 1-3 business days. Clean tax documentation too.

- Rise (formerly Riseworks). The industry-standard processor, works with almost every firm. EUR payouts to your German bank in 3-5 business days. Expect roughly $10-20 conversion spread on a $1,000 payout.

- Crypto (USDT/USDC). Fast, usually same day, but adds tax complexity. You owe tax on the EUR value at receipt, and converting later can create a second taxable event. Document everything.

- PayPal. Convenient, but the USD-to-EUR conversion costs 3-4%. Fine for small payouts.

- Wise. Near-interbank rates and a clear paper trail. Often the best option when offered.

| Prop Firm | Payout Methods (DE) | EUR Payouts | Best For |

|---|---|---|---|

| Lucid Trading | SEPA, Rise, Crypto | Yes (SEPA) | Futures, best payout terms |

| FundedSeat | SEPA, Rise, Crypto | Yes (SEPA) | Futures, fast evaluations |

| Top One Futures | Rise, PayPal, Crypto | Via Rise | Futures, aggressive traders |

| FundingPips | Rise, Crypto | Via Rise | Forex, funded fast |

| YRM Prop | Rise, Crypto | Via Rise | Futures, simple rules |

| Breakout | Rise, Crypto | Via Rise | Crypto, Kraken-backed |

| Hyrotrader | Rise, Crypto | Via Rise | Crypto, low cost entry |

One thing to know upfront: almost no prop firm offers German-language support. Dashboards, FAQs, and tickets are all in English. That's rarely a problem in practice, and FundingPips has fast live chat used to non-native speakers. The trading itself can still be partly in German: NinjaTrader and TradingView both have German interfaces. Rithmic is English-only.

My Recommended Setup for German Prop Traders

After years of trading from Germany and collecting payouts from a dozen firms, here's what works best:

- Pick a firm with SEPA or Rise payouts. Lucid Trading for futures, FundingPips for forex. If you're starting from zero, here's the full path to becoming a funded trader.

- Open a dedicated bank account (N26, Vivid, or a second Sparkasse account) exclusively for prop trading income and expenses. Tax documentation becomes trivial.

- Track every evaluation fee. A simple spreadsheet: date, firm, USD, EUR, passed/failed. That's your Werbungskosten documentation at tax time.

- Find a Steuerberater before your first payout. The €200-500 consultation saves you from classification mistakes you'd spend years correcting.

- Set aside 35-40% of every payout for taxes. For most German traders with a day job plus prop income, the effective rate lands in the 33-42% range. Better to overestimate and get a refund than face Nachzahlungszinsen from the Finanzamt.

The bottom line: BaFin doesn't regulate your challenge accounts. Your payouts are most likely sonstige Einkünfte at your personal income tax rate. And you probably don't need a Gewerbeanmeldung unless prop trading becomes your primary income. Lucid Trading for futures and FundingPips for forex are my picks, with FundedSeat, Top One Futures, and YRM Prop as reliable alternatives. The tax question isn't scary. It's just unfamiliar.

Frequently Asked Questions

Is prop trading legal in Germany?

Yes. No German law prohibits residents from participating in funded trader evaluation programs offered by international prop firms. BaFin does not regulate these programs because they involve simulated accounts, not regulated financial products. You can sign up, trade, and collect payouts from any firm that accepts EU residents.

How are prop trading payouts taxed in Germany?

Most commonly as sonstige Einkünfte under §22 EStG, at your personal income tax rate (14-45%). The flat 25% Abgeltungssteuer (§20 EStG) typically does not apply because payouts are performance-based contractual payments, not returns on invested capital. Confirm the classification with a Steuerberater.

Do I need a Gewerbeanmeldung to trade with a prop firm in Germany?

Most German prop traders don't. The requirement triggers only when the Finanzamt classifies your activity as a Gewerbe based on volume, frequency, and revenue consistency. Occasional payouts typically fall under §22 EStG as sonstige Einkünfte. Above roughly €2,000/month of consistent income, have a Steuerberater evaluate registration.

Is the Abgeltungssteuer (25% flat tax) applicable to prop trading income?

Almost certainly not. The flat 25% capital gains tax covers returns on personally invested capital in regulated brokerage accounts. Prop firm payouts are performance-based contractual income from a simulated trading arrangement, not investment returns. Expect your personal progressive income tax rate (14-45%) instead.

Can I deduct evaluation fees on my German tax return?

Yes. Evaluation fees are deductible as Werbungskosten when reporting under §22 EStG, including fees for failed evaluations, since they're directly related to earning the income. Data feeds, trading software, and platform costs are deductible too. Deductions must exceed the Pauschbetrag before they provide additional benefit.

Do I owe VAT (Umsatzsteuer) on prop firm evaluation fees?

Not as a private individual without a Gewerbeanmeldung. Reverse-charge VAT obligations don't apply to private persons. Traders with a registered Gewerbe and USt-IdNr self-assess VAT under §13b UStG but immediately reclaim it as Vorsteuer, a net-zero impact.

Which prop firms offer SEPA payouts to German bank accounts?

Lucid Trading and FundedSeat are among the firms supporting direct SEPA payouts to European bank accounts, depositing EUR straight into a German Girokonto without conversion fees. Most other firms process payouts through Rise (formerly Riseworks), which also supports EUR transfers to German banks with a small conversion spread.

What records should I keep for the Finanzamt?

Payout statements from every firm, evaluation fee receipts (including failed attempts), bank statements, the firm's terms of service, and a brief description of the business model in German. Use ECB reference rates for USD-to-EUR conversion. A dedicated bank account simplifies everything.

How much should I set aside for taxes on prop firm payouts in Germany?

Reserve 35-40% of every payout. The effective rate depends on total income within the progressive 14-45% range. A trader with a €50,000 salary plus €20,000 in annual prop payouts faces a marginal rate around 42% on the prop portion. Quarterly Vorauszahlungen prevent large year-end bills.

Should I trade from Germany or move to a lower-tax country?

Trading from Germany works well for the vast majority of prop traders. Access isn't restricted by EU country, and relocating to Switzerland, Dubai, or Portugal only makes financial sense above roughly €100,000 in annual prop revenue. Optimize your German setup first: correct classification, full deductions, proper Vorauszahlungen.